If ever a football club’s season could be described as the proverbial “game of two halves” that would be the one experienced by Liverpool fans this year. Following Roy Hodgson’s appointment as manager last July as the replacement for the popular Rafael Benitez, the Reds endured their worst league start in more than 50 years, falling into the relegation zone in October after a dismal home defeat to newly promoted Blackpool.

Hodgson’s grim tenure came to an end in January, when he was replaced by Kenny Dalglish, who inspired a revival that took Liverpool back up the table to sixth place. Moreover, the team threw off the shackles and played some sparkling football, including wins over Manchester United, Chelsea and Manchester City. Although Dalglish’s record in his previous reign on the Mersey was highly impressive, winning three league titles and two FA Cups, some had expressed doubts about the Scot’s credentials, as he had not managed a club for more than a decade and he was initially appointed on a temporary basis.

However, the mood at Anfield has clearly taken a massive turn for the better and virtually all of the non-believers have now been converted. Thus, it was no surprise that Dalglish was duly confirmed as permanent manager a couple of weeks ago, when he was given a three-year contract along with his first team coach Steve Clarke. As new owner John W Henry said, “Kenny is a legendary figure, both as a supremely gifted footballer and successful manager.”

"John W Henry - the man with a plan"

The new ownership is, of course, the other vital change to occur at Liverpool during this momentous season with New England Sports Ventures (NESV) taking over from the reviled pair of Tom Hicks and George Gillett last October. Well known for its stewardship of the Boston Red Sox, one of the most famous baseball teams, and involvement in NASCAR, the company has now changed its name to the Fenway Sports Group (FSG), but the key executives remain the same. As far as Liverpool are concerned that means John W Henry, the principal owner, and Tom Werner, the chairman, who both hold 50% of the voting rights in the football club.

They look like a good fit for Liverpool, as explained by the club’s former chairman Martin Broughton, “New England have a lot of experience in developing, investing in and taking Boston Red Sox - as the closest parallel - from being a club with a wonderful history, a wonderful tradition that had lost the winning way, and bringing it back to being a winner.” In fact, after buying the Red Sox in 2002, NESV delivered success just two years later, as they won the World Series in 2004, ending an 86-year wait for honours, and then repeating the feat in 2007.

On the face of it, they could not be more different to their unpopular predecessors, Hicks and Gillett, who saddled Liverpool with a mountain of debt when they bought the club in March 2007. Ever since then, the Reds had been on a financial knife edge. Even though the eternally optimistic former managing director Christian Purslow claimed that he could not “conceive of a situation where Liverpool Football Club could go into administration”, the reality was that the choice had been taken out of his hands.

"Luis Suarez - happy days"

The club’s bank loans were due for repayment in January 2010, but the club failed to make the £250 million payment, and the club only survived when the bank extended the date first to March and then by a further seven months to October to facilitate the sale of the club. Liverpool’s auditors KPMG had gone public with their concern over the level of debt the previous year, when they described the issue as “a material uncertainty which may cast significant doubt on the group’s and parent company’s ability to continue as a going concern.”

UEFA were also well aware of Liverpool’s financial difficulties. Last month William Gaillard, Senior Advisor to UEFA President Michel Platini, spoke about them, while warning football dignitaries of the dangers of leveraged buy-outs, “The club has been rescued, thank God, but it was a close call. They suddenly found themselves being owned by two failed banks that had been taken over by governments.”

In fact, the Royal Bank of Scotland (or indeed Wachovia) could have put the club into administration (with a nine point penalty) at any time in the last few months of the Hicks and Gillett regime. Importantly, this meant that RBS could dictate terms, allowing them to place Purslow and commercial director Ian Ayre on a reconstituted board, while stipulating that the owners could no longer appoint new representatives to the board. This meant that when the decision to sell the club was taken, Hicks and Gillett no longer had a majority, so could be outvoted by the other board members.

"Keep calm and Carra on"

Even though he is from Texas, Tom Hicks did not know when to “fold them” and tried to block the sale, describing the transaction as “an epic swindle at the hands of rogue corporate directors.” So RBS brought a legal action before the High Court to obtain a judgment on the ability of the new board to complete the sale to NESV, which they duly won. Even the elegant Broughton could not resist putting the boot in, describing the former owners’ actions as “a flagrant abuse of their undertakings.”

Acting on behalf of the club, Barclays Capital had contacted 130 potential investors, but only two bids had been received before the deadline with NESV’s winning out. They paid a total of £300 million for the club: £218 million for the equity, effectively the amount that Hicks and Gillett owed to RBS, and £83 million to assume responsibility for other debts. This was a pretty good outcome for the club, as the acquisition debt was wiped out, leaving NESV with more funds to spend on the football side of the club – and it had the added bonus of serving up a side order of schadenfreude, as Hicks and Gillett lost their £144 million investment.

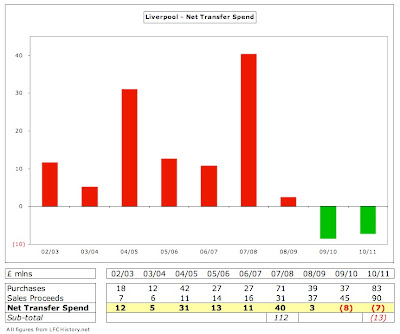

The last accounts published under the old administration reflected the club’s financial shortcomings, as they reported a £20 million loss, which was £6 million worse than the previous year, even though profit on player sales rose dramatically from £4 million to £23 million, mainly due to the sale of Xabi Alonso to Real Madrid. The wage bill climbed an incredible 18% to £113 million, which was much higher than the 4% revenue growth.

That said, for the last two years, Liverpool have only made a small loss before interest payments, £2.3 million in 2010 and £3.5 million in 2009, but the impact of interest on the loans that Hicks and Gillett took out to buy the club has been hugely detrimental with net interest payable increasing from £13 million last year to £18 million in 2010.

However, that’s not the whole story, as these are only the accounts for The Liverpool Football Club and Athletic Grounds Limited, while the majority of the club’s debt was held in the holding company. Unfortunately, the 2010 accounts for Kop Football (Holdings) Limited, the largest group company incorporated in the UK, have not yet been published, but we do know that the net interest payable at that level in 2009 was a whopping £40 million, leading to a net loss for the group of £55 million. If we make the reasonable assumption that the level of interest in 2010 is the same, this would mean that the club had paid around £125 million of interest during Hicks and Gillett’s unhappy reign.

Another interesting point is the large amounts paid out for changes in management, which amounts to £12 million in the last two years, including around £8 million for Rafael Benitez and his coaching staff in 2010 and £3 million compensation for directors’ loss of office in 2009 (reportedly Rick Parry).

In fact, Liverpool have only made a profit once in the last five years, specifically 2008, when they registered an £8 million surplus, largely due to £22 million profit on player sales, after a number of experienced players were moved on (Crouch, Sissoko, Carson, Riise and Guthrie). However, the new Premier League deal was also an important contributory factor, leading to a £16 million rise in television revenue.

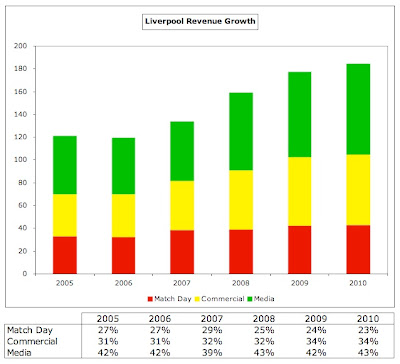

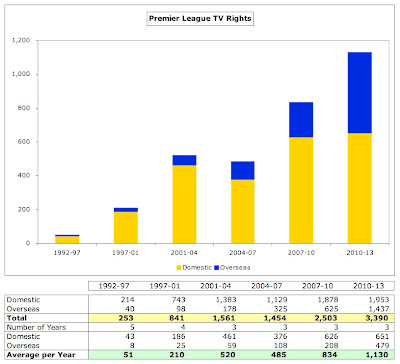

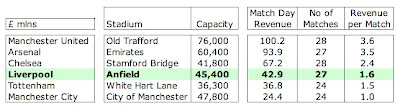

Like all football clubs, the additional riches provided by the ever-increasing TV deals has been a critical factor in Liverpool’s revenue growth, contributing almost half (£29 million) of the £64 million rise in turnover since 2005. However, the fastest growing activity is commercial income, which has risen an impressive 68% in the same period. Match day revenue has also grown from £33 million to £43 million, but remained relatively flat compared to the other revenue streams. On the plus side, Liverpool’s revenue is fairly evenly distributed among the three main revenue streams, which means that they are not unduly reliant on one area.

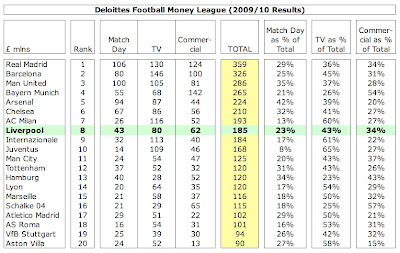

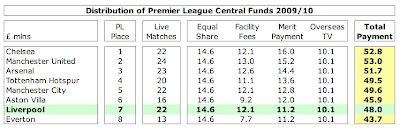

There are a couple of ways to look at Liverpool’s revenue of £185 million. On the one hand, this puts them in a more than respectable ninth place in the Deloitte’s Money League, which ranks clubs in order of revenue, but, on the other hand, they are still a long way behind the clubs at the top of the (money) tree. In particular, the Spanish giants generate considerably more income with Real Madrid and Barcelona earning £359 million and £326 million respectively, approaching twice as much as the Reds. Moreover, bitter rivals Manchester United earn £100 million more than Liverpool every season, which is a considerable competitive advantage.

Furthermore, Liverpool dropped a place in the Money League last season and can expect a further decline next year, as they will not have the benefit of Champions League revenue, while Manchester City’s commercial revenue is likely to climb again under their Middle East owners. This would mean that four English clubs will receive more money than Liverpool (United, Arsenal, Chelsea and City), which would be a concern, unless the new owners can address the club’s weaknesses.

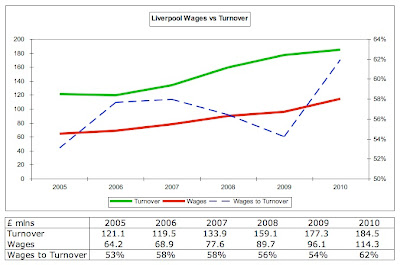

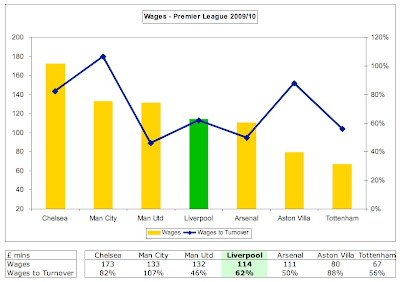

One obvious issue is the wage bill, which has soared to £114 million, up from £96 million the previous year, mainly due to contract extensions. This has increased the important wages to turnover ratio to 62%, the first time that it has gone above 60% in that period. In fairness, this is still below UEFA’s recommended maximum limit of 70% and is much better than most other clubs in the Premier League, notably big-spending Manchester City (107%) and Chelsea (82%). What is worrying, however, is that performance on the pitch has worsened, while the wage bill has risen, which is the opposite of what usually happens in football, culminating in the team failing to qualify for the lucrative Champions League.

That was then, this is now.

The recently appointed managing director, Ian Ayre, described the results as “a footnote in our history”, as he suggested that the club was now “moving forward.” It is entirely appropriate that we concentrate on the new owners’ future strategy, not least because John W Henry made his fortune as a futures trader.

Actually, I say “fortune”, but everything’s relative. While his estimated worth of £375 million might be enormously impressive to the proverbial man in the street, it’s small change compared to the billions owned by other prominent owners of football clubs, such as Sheikh Mansour, Roman Abramovich, Stan Kroenke and even the Glazers. It’s actually even lower than the likes of Peter Coates at Stoke City and David Sullivan at West Ham.

Therefore, Liverpool fans should not expect a classic sugar daddy. Instead they have got a group of savvy businessmen with proven expertise and a superlative record in sports management. Nevertheless, the new owners will still need to access substantial funds in order to strengthen the squad and address the stadium situation (either build a new stadium or redevelop Anfield), so the obvious question is how will this be financed? Liverpool fans would not want to see the club take on large levels of debt once again, so Henry’s team really has to address the club’s faltering business model.

Although we are not privy to their strategic plan, we can make some fairly good guesses at where they will try to turn around Liverpool’s finances, based on their announcements to date, which I have attempted to summarise in a 15-point plan.

1. Put your shirt on it

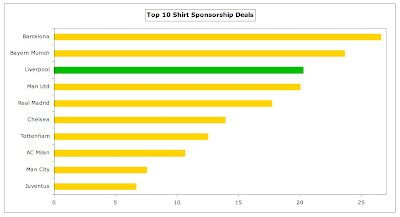

While discussing the most recent financial results, Ian Ayre stated, “We have had significant commercial growth since these accounts were published.” He can point to the shirt sponsorship deal with Standard Chartered starting next season, which “can generate up to £81 million” over four years. Although it is understood that some of this may be performance related, this implies £20 million per annum, which is £12.5 million higher than the current deal with Carlsberg. This is in line with Manchester United’s Aon deal, but Barcelona’s £25 million deal with the Qatar Foundation has raised the bar again - even higher than Bayern Munich’s £24 million deal with Deutsche Telekom.

Last month it was reported that Liverpool had secured a £25 million kit deal with Warrior Sports, a subsidiary of New Balance, from the 2012/13 season, though this has not been officially confirmed. This is an example of the synergy that FSG can bring to the party, as Warrior recently announced a deal to manufacture kit for the Red Sox. The deal would more than double the amount received from Adidas, who currently pay £12 million a year. Although the press reported this as a record for English football, it is actually slightly lower than Manchester United’s Nike deal, which had a contractual step-up from £23.3 million to £25.4 million this season, but it’s still a mighty impressive increase.

In total, the two shirt deals will deliver a substantial revenue increase of around £25 million a season (Standard Chartered £12.5 million, Warrior £13 million).

2. Going global

Liverpool’s commercial income of £62 million is already pretty good, being sixth highest in the Money League, though it is only half the amount earned by Bayern Munich and Real Madrid and it actually fell last year if you consider that LiverpoolFC TV Ltd was brought in-house in July 2009. In fact, Liverpool sell more shirts than any other club except Madrid, Barcelona and United.

An important element of the club’s strategy is therefore to “leverage the club’s global following to deliver revenue growth”, which Tom Werner emphasised, “We consider Liverpool to have untapped potential globally.” This is clearly one of the key drivers for American investors, as explained by Don Gerber, head of Major League Soccer, “There’s a belief that there’s a valuable global franchise with these clubs.”

In particular, Werner has stated that the club is focused on Asia (“The support the club has there is already considerable”), hence the pre-season tour to China and South Korea. However, this has lead to club sponsor Standard Chartered, who make much of their income in Asia, somewhat crassly suggesting that they would like Liverpool to sign players from that region, citing the example of Park Ji-Sung at United.

Liverpool fans would have been equally perplexed at the news that basketball star LeBron James had bought a stake in the club, but this is part of his marketing deal with FSG and has helped raise Liverpool’s profile in the States.

More worrying is Ian Ayre’s apparent support for the 39th game, a proposal to play an extra round of Premier League matches at neutral venues outside England: “We have a duty to fans around the world to give them access to the product.” I’m not sure that the fans on the Kop would necessarily agree with that sentiment.

Comment